If you’re starting a business or already running one accepting only cash, you should know that research shows purchases with cards outdo cash purchases by a huge percentage. A 2023 survey from Forbes Advisor shows that 90% of customers purchase with a card, whether debit or credit.[1] Forbes. “Credit Card Statistics And Trends.” Accessed April 16th, 2025. This means less than 10% of customers primarily purchase with cash. Accepting a variety of payments allows your business to reach more prospective customers, making it a potentially lucrative practice. If you’re running any kind of business, accepting credit card payments specifically is a necessity for your enterprise to thrive.

Ready to learn how to accept credit card payments? Below, we discuss everything you need to know to set up credit card processing for your business.

Key Takeaways

- The three main ways to accept credit card payments are online, in-person, and over the phone.

- Setting up credit card processing involves contacting a merchant service provider, determining your method of payment acceptance, applying for a merchant account, setting up POS hardware, and implementing chargeback prevention and management tools.

- The benefits of accepting credit cards include increased sales and credibility, improved customer experience and security, and international reach.

Different Ways To Accept Credit Card Payments

There are three ways to accept credit card payments: online, in person, or over the phone. Each method requires its own tools to successfully complete payment transactions.

How To Accept Credit Card Payments Online

Accepting online credit card payments comes with a variety of benefits. It allows you to take payments from customers across the globe. This is especially relevant, as research from 2024 shows that 52% of online shoppers buy internationally. [2] Forbes. “35 Top E-Commerce Statistics” Accessed April 16th, 2025.

Additionally, taking credit card payments online provides your customers with a quick and smooth checkout experience. It also helps you stay competitive, as other businesses are likely already offering this payment option.

To start processing credit card payments online, you need these three elements:

- An online storefront – This allows you to display your products or services to browsing customers. To sign up for a digital storefront, many businesses simply create an account through an eCommerce platform provider.

- A payment gateway – A payment gateway provider enables your business to integrate a cart and storefront, giving you the ability to process payments through a secure, cloud-based solution. With this software, it’s simple to get up and running.

- A payment processor – Your processor will collect customers’ payment information and communicate that data between your merchant account and the banks involved. It ensures the funds are authorized and approved, then transferred from the customers’ issuing bank to your merchant account.

How To Accept Credit Card Payments in Person

Taking in-person credit card payments also offers advantages. Since about 41% of in-store transactions use credit cards, accepting card payments allows you to cater to a significant portion of the market. [3] Capital One Shopping Research. “Cash vs Credit Card Spending Statistics.” Accessed April 16th, 2025 Offering this payment option provides customers with more convenience, improving customer satisfaction and likely boosting sales.

To complete in-person transactions, you’ll need a payment provider to handle processing your credit card payments for you. Some merchant service providers, like PaymentCloud, can help get you the right hardware for your needs. You’ll also need a point-of-sale (POS) system. This system includes all the necessary hardware, like a credit card reader, as well as the software that processes the credit card information.

Types of hardware you can use include:

- Countertop card readers: These are card readers merchants use at their store counters and are attached to a larger POS system, often with guest display and merchant screen. They work best for businesses like restaurants, bakeries, ice cream stores, pizzerias, or frozen yogurt stores. They can support NFC payments, EMV payments, and Magnetic Stripe Reader payments.

- Mobile card readers: These are handheld card readers merchants can carry with them. They work best for taking orders from anywhere inside or outside a restaurant and accepting takeout and curbside payments.

How To Accept Credit Card Payments Over the Phone

Merchants may want to take MOTO payments or Mail Order Telephone Payments. The term is a misnomer since most businesses don’t do mail orders, but the acronym is still used to describe over-the-phone transactions. This option is often a must for businesses like restaurants, caterers, and catalog-based businesses. This gives customers the option of paying over the phone, making the process more convenient and increasing the likelihood of repeat business. In fact, 63% of customers are more willing to shop at businesses that offer the payment method they prefer. [4] CIO. “Consumers Want More Payment Flexibility in Their Shopping Experience.” Accessed April 16th, 2025

It’s also an efficient sales funneling method because you can better encourage the customer to complete their purchase if they call with any issues.

To accept credit card payments over the phone, you’ll need a virtual terminal. With this, you can manually enter the customers’ card information online, including the card number, CVV, and address, to verify authenticity. For example, a construction contractor can pay for materials from their admin office over the phone, so a subcontractor can easily pick the supplies up without needing access to sensitive payment information. The merchant can also initiate invoices from the virtual terminal interface.

How To Set Up Credit Card Payments for Your Business in 5 Easy Steps

Here’s a summary of the five steps needed to set up your business for credit card payments.

1. Contact a merchant service provider

Some providers allow you to sign up online, while others require you to contact a sales representative. After that, you can negotiate a contract. Some may require you to print out an application and scan it with a physical, handwritten signature.

2. Determine how you will be accepting credit card payments

Next, decide which payment methods you’ll want to accept. As noted, your options include credit card payments online, in person, or over the phone.

3. Apply for a merchant account

Once you’ve reviewed the available payment options and are ready to apply for a merchant account, here’s what you need to know:

A merchant account is a channel set up with a bank to process electronic credit card transactions. This has been the traditional way in which businesses accept card payments. Merchant accounts function much like a holding account for your business. Money from card purchases goes into your merchant account, where it is held until the transaction is complete. Then, the funds are transferred to your bank account.

Merchant service providers range from banks and payment processing companies to independent sales organizations (ISO). Hundreds of providers exist in the market.

Applying for a merchant account may seem complex, but there are helpful guides on setting up a merchant account to make the application process easier to navigate. Here is an overview of steps to follow before hitting “submit” on your merchant account application:

- Obtain a business license

- Establish a business bank account

- Confirm your business structure

- Consider separate processors

- Add terms of service and refund policies

- Ensure PCI compliance

- Gather required documents

Once you complete your application, most often online, a merchant services provider will review your documents and grant your approval. At this stage, there are a few final steps to take to prepare your business for its new processing features.

4. Set up hardware and/or software integrations

Depending on your business’s payment options, you’ll need different equipment and software. For example, for online processing, you will not need a countertop credit card terminal or POS system with physical hardware required for in-person transactions.

Your new processing may mean that you have to upgrade and integrate your existing software and/or hardware. If your business is a brick-and-mortar, you might have to buy checkout software or install an EMV chip-enabled card reader. Your payment service provider may supply this equipment for you.

5. Secure a reliable chargeback prevention and management tool

As a final step in your credit card processing journey, set up chargeback prevention and management tools if you’re taking payments in an online or card-not-present environment. A chargeback is a payment that is returned to a customer’s card due to a charge dispute or a return. Because chargebacks can be costly to your business, you should be proactive about preventing and managing them. Make sure you invest in effective transaction recordkeeping, quality customer service, and chargeback management solutions.

With effective systems in place to manage all your processing needs, you can set your business up for financial health and credit card processing success in the future.

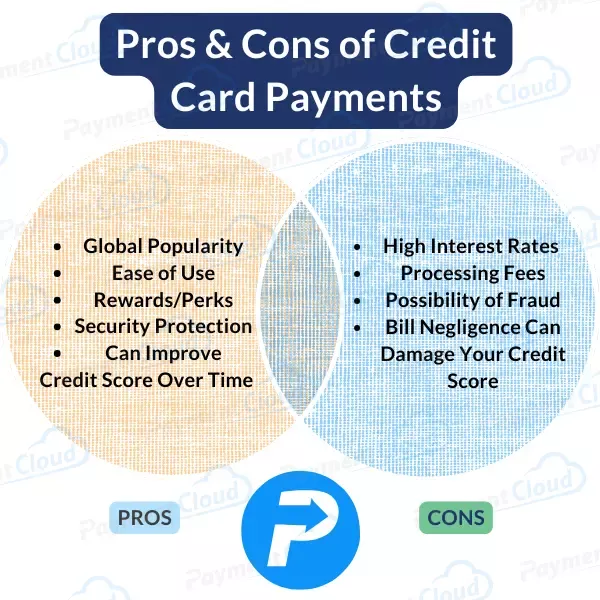

Benefits of Accepting Credit Cards

The benefits of accepting credit cards include:

- Allowing you to take payments from customers internationally

- Empowers you to keep up with your competitors

- Encourages customers to make larger purchases at your business since they’re not limited by the physical cash they have

- Offers your customers a quick and convenient way to pay

- Increases the likelihood they’ll come to you again

How Can I Accept Credit Card Payments? Closing Thoughts

By now, you should have a good understanding of how to take credit card payments for your business.

Accepting credit card payments immediately improves your business by helping you reach more customers. In today’s world, the average consumer is looking for quick and convenient ways to shop. By accepting credit cards, your business can appeal to modern consumer behavior and boost your sales. PaymentCloud offers you credit card processing solutions using innovative technology, quick processing, competitive rates, and 24/7 merchant support to make accepting credit cards simple. Reach out to us today to see what we can do for your business!

Ready to accept payments? Have your merchant account up and running in no time.